Joe DiRollo, Founder and CEO, ALMIS International

Central banks around the world are assessing and developing improved ways to receive and analyse data from banks. Since the 2008 banking crisis, there has been a tsunami of regulations and reporting requirements for Banks and, bluntly, the banking industry has struggled to keep up with these frequent and ever more complex requirements.

The Bank of England and Financial Conduct Authority, for example, embarked on a significant project to transform data collection from the financial sector, the aims of the project include.

- Having a common data standard for the industry

- Modernising the reporting instructions

- integrating the reporting approach

Banks have to remain transformative in terms of their reporting procedures, however many continue to rely on spreadsheets and manual processes in order to pull together the information necessary to satisfy the Board and Regulators.

They struggle to meet the deadlines and internal audit reports worry Executives, Boards and Regulators and highlight the necessity of a modern and holistic approach. The stark reality is that this is overdue, is becoming the fact it is overdue is almost universally recognised.

In its simplest form rather than sending individual completed reports on say Credit Risk by Country – firms will send the dataset in a more granular form so that risk metrics and analysis can be computed, from the institution’s perspective its one detailed submission of core data. Whilst regulators gain access to market wide and individual firm analytical capabilities which allows far greater analysis.

In my opinion, these aims are laudable and exactly what is needed, whilst acknowledging that there is real difficulty in delivering this.

Numerous legacy systems coupled with the simple fact there is no ‘one size fits all’ and a mixture of simple and highly complex business models, instruments, and balance sheets. Standardisation whilst achieving the requisite granularity is a very difficult undertaking, perhaps part of the reason that no one has succeeded.

Following the aforementioned crisis, and BASEL and CRR reforms, we’re now seeing a massive uptake in the use of our technology to provide the necessary answers to these ongoing and increasing demands. Indeed, ALMIS is carrying out comprehensive groundwork to grow in line with the complexity of these regulatory demands.

The enhanced data model has been engineered to facilitate both current and expected future requirements for Regulatory Reporting and Middle Office plus has been developed to wrap around the data model and help institutions bring in and manipulate data within the software and remove the need for manual or external data manipulation.

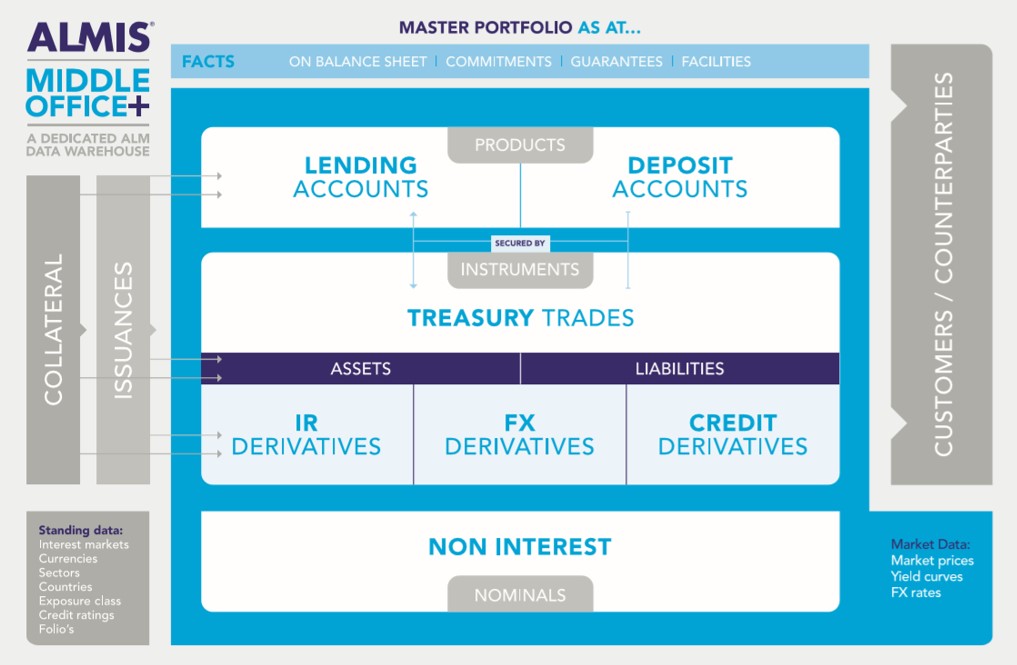

Building on a heritage of traditional asset liability management protocols, ALMIS Middle Office + works by bringing in detailed end of day data and ensuring that the truth data reflects the full balance sheet, so you have the whole truth. The centre piece of this is the data model of course and how it is organised.

Lending, Deposits and Treasury trades should not be normalised because they are all hugely different business activities. Each therefore has its own data elements or table. Liabilities can be secured against assets, so these links are inherent to the model. Collateral is attached to assets with its own dimension elements. The data model reflects the need for a customer view across all accounts and trades, and a product or instrument view.

They key here is to take a complete snapshot of all relevant on and off-balance sheet data as this ensures the information is used both in the Regulatory Reporting and the firms internal ALM analysis is complete, and it also builds validation into the process by design.

Crucially reporting to the Regulator is not a Silo activity. The same data, data model and tools are used for all the necessary Board and Committee analytics ensuring the senior management and the Regulators views are aligned and the information they receive is both correct and consistent.

In conclusion, banks around the world have been critical of regulators constant demands for complex and changing reporting requirements and often do not see how providing all this information, at a high cost to themselves, provides much any benefit to them or the industry.

Regulators are actively responding to this and looking to improve and modernise how reports and data are collected. Currently these projects are at a very early stage, and no one yet has found the answer.

However, to solve this, we believe regulators must start looking at how to address this for the less complex institutions and build a solution from there. Solve and prove it for the simplest firms and then scale upwards.