Arjun Nagaraj, Operations Director, RIGHTCARE RIGHTNOW PVT LTD

Cost management plays an important role in the process of planning and controlling the budget of a business entity. Cost management allows a business entity to predict impending expenditures to benefit with reduce in excess budget. For any organization, the major objective is to maximize their profit; but the major obstacle facing them are the rise in cost of operation, production and logistics. Cost Management can be observed in all industry like Transportation, Telecommunication, Agriculture, Construction, Health care, Hospitality, Entertainment, Media Industry, Manufacturing and so on.

Today businesses are too competitive, impacting every organization. A spontaneous reaction under the current circumstances is just to cut all the costs to the minimum level. For which every aspect of an organization’s cost structure must be examined carefully to reject unnecessary and non-value adding expenditure, while retaining its competitive position in the market.

Cost reduction, process will not only imply on operation cost but even includes non-operational costs, fixed costs and Variable Costs as well.

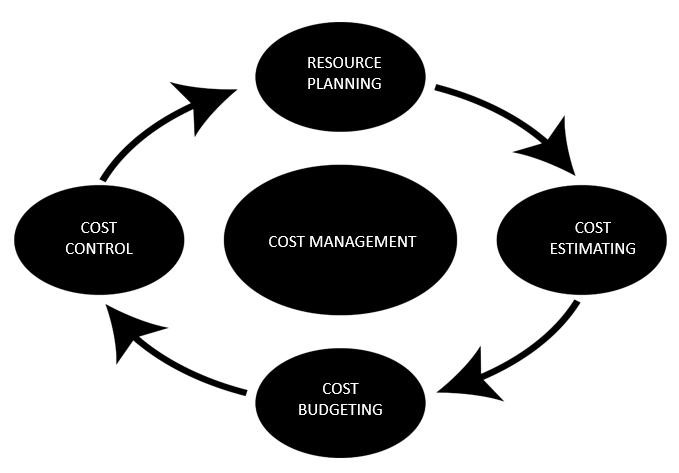

Cost management is usually a process with is inter related and can be done in following methods’

RESOURCE PLANNING

This process can be determined as an initial phase of an organization/project which plays an important role. This process of defining the requirements in an organization or required resources to complete the project in a Work Breakdown Structures (WBS) and historic data of projects can be utilized to outline the requirements. You can chart down the specific mandatory things like required time, labor, equipment and materials etc. Once the requirement types and quantities are known the associated costs can be determined.

COST ESTIMATION

Cost estimating methods can be implemented in several ways to forecast the cost required to perform the operations in an organization or to complete the project. Cost estimation is more related to planning while planning it is to be included what are the requirements and projection of future requirements. Estimating in appropriate of over-all cost of the resources and requirements for completing the project would make it easier and simpler in estimating the budget.

You can chart down the specific mandatory things like required time, labor, equipment and materials etc. Once the requirement types and quantities are known the associated costs can be determined. Another possibility is to use parametric models in which the characteristics are statistically represented. Estimates can be refined when information becomes available during the development of a project.

COST BUDGETING

Cost budgeting involves gathering the costs of individual activities or work packages to begin a total cost baseline for computing project performance. The project/Business budget provides and overview of the periodic and total costs of the business requirement. Cost budgeting usually occurs after the cost estimating. Various projects start with a total budget before the basic requirements of a project are identified, but in many cases, these specific budgets may be reexamined after cost estimation occurs.

Cost budgeting techniques

- Parametric estimating: This is generally essential when the project is in the conceptual or Initial stage of development and the details of the project are not known. For the further phase, the required detail will be shaped only as a result of the current work.

- Funding limit reconciliation: The timing of funds and planned costs for projects must solve two problems: solvency and fiscal timing with-respect to Cost baseline; Project requirements; Keep posted to the cost management plan;

- Cost baseline: The prime goal of cost budgeting process is to obtain the cost baseline. Once the budget is approved, it marks the baseline.

- Project funding: Requirements can be derived from project baseline and will cover all the project expenditures.

Furthermore, to keep a hold on budgeting could be done in following ways

1. Keeping the budget up-dated: The process is updated with change requests that could affect the administration of costs.

2. Cost budget reserves: Reserves analysis is a Cost Budgeting method used to identify the areas which are in need of reserves. Budget allocations provide challenges to individual accounts as below. In order to moderate the risk of insufficient resources, it is suitable and helpful to create a cost reserve.

Types of reserves that could be created

- Contingency reserve

- Management Reserve

- Parametric estimating

Cost Control

Cost control is the practice of recognizing and reducing expenses to increase profits which is related to budgeting process. Procedures applied to monitor expenses and performance in contradiction of the progress of the business project. All variations to the cost baseline need to be recorded and analyzed to understand the entire costs that further needs to be forecasted.

When actual cost data becomes accessible, a significant part of cost control is to clarify what is causing the variance from the cost baseline. Based on this analysis, counteractive action plan might be required to avoid cost overruns. Tightening cost control provides an organization / business entity with extensive impact over their cash flows and increased trended revenues. There are ways to control cost by understanding the factors and analysis of the outcome.

- Budget Prospective is a process where the budgets are used as a means of planning and controlling costs. It includes the process of preparing budgets and co-coordinating all the departments, comparing real-time performance with the budget allocated and acting upon the results to achieve maximum profitability.

- Standard Prospective is a process where cost of an end-product / Service is pre-calculated based on normal levels of operation. The actual cost and Variable cost are compared and if any deviation or variance is ascertained, an analysis of variance is made with reference to their causes.

- Material Prospective is a process where cost of material which constitutes a large proportion of the total product / Service cost. The Purchase of Materials that needs to be closely observed and ensured that the required quantity and quality of material required with minimizing amount of capital investment.