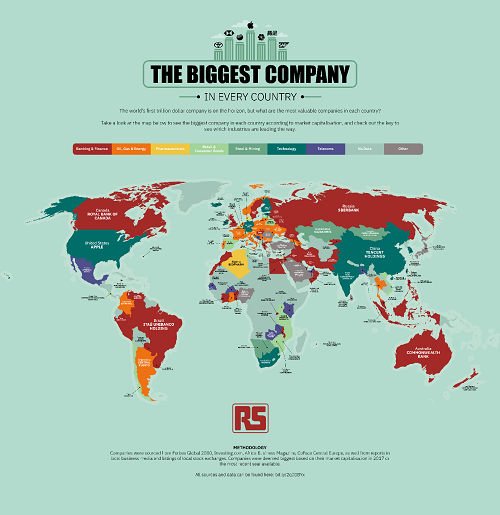

Big business is booming around the world, with companies like Apple, Tencent and Samsung posting billions in profits every year. But not every company on the world’s stage is as well known. Take a look at the map below to see the biggest company, according to market capitalisation, in over 100 different countries around the globe.