By Michael Levens, Global Head of Payments at Delta Capita

…but you must act now to get the benefits. As a financial institution, now is time to start engaging with payment infrastructures around adoption of the incoming international standard ISO 20022.

In November 2022, this new standard for data exchange will transform the global financial services industry. It will unlock huge opportunities for financial institutions, such as boosting operational efficiency, enhancing customer experience, and enabling innovative new services.

ISO 20022 creates a common language for payments worldwide through an open standard for electronic data interchange between financial institutions. Better data will mean better payments for all.

But, for successful adoption, institutions will need to know how payment market infrastructures plan to adopt the standard and how they will interact with these infrastructures.

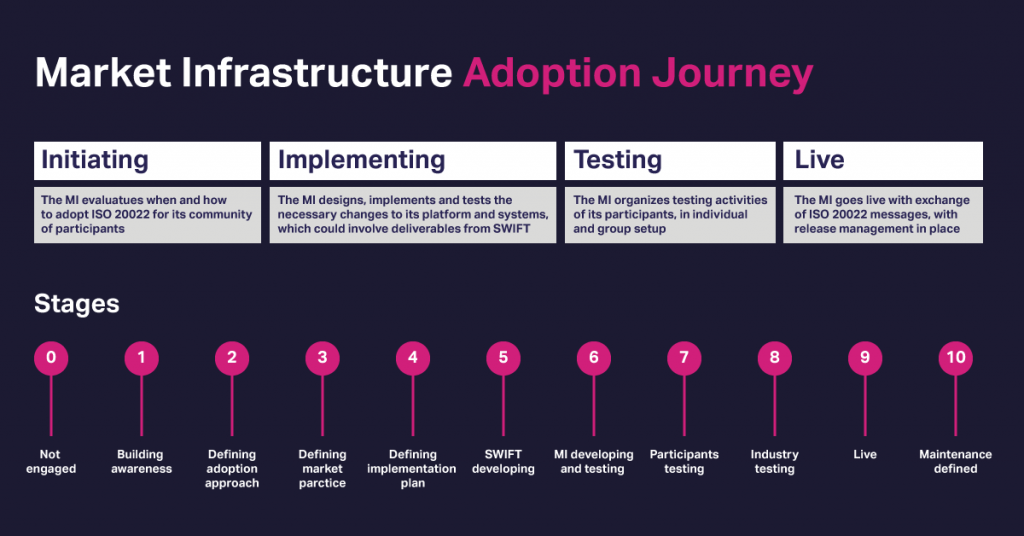

What are payment market infrastructures (MIs)?

MIs are pivotal to the financial system – they are the structures that provide financial institutions with centralised transaction processing, allowing higher efficiency, and lower costs and risks.

Typically, MIs establish rules, procedures, and risk management frameworks for all participants and use a shared technical infrastructure. The three main MI types cover: payments; securities; and foreign exchange and treasury infrastructures.

Payments MIs systems break down further into ones that handle low-volume, high-value transactions (HVPS) and those managing high-volume, low value (LVPS) – ISO 20022 applies to both.

Low value transactions are made through automated clearing houses, which allow for ISO 20022.

For high value transactions, global banks and MIs have joined SWIFT, the global financial messaging network, to form the HVPS+ Market Practice Task Force. This promotes stable best practice and harmonisation around ISO 20022; and reduces the risk of fragmentation due to market inconsistencies.

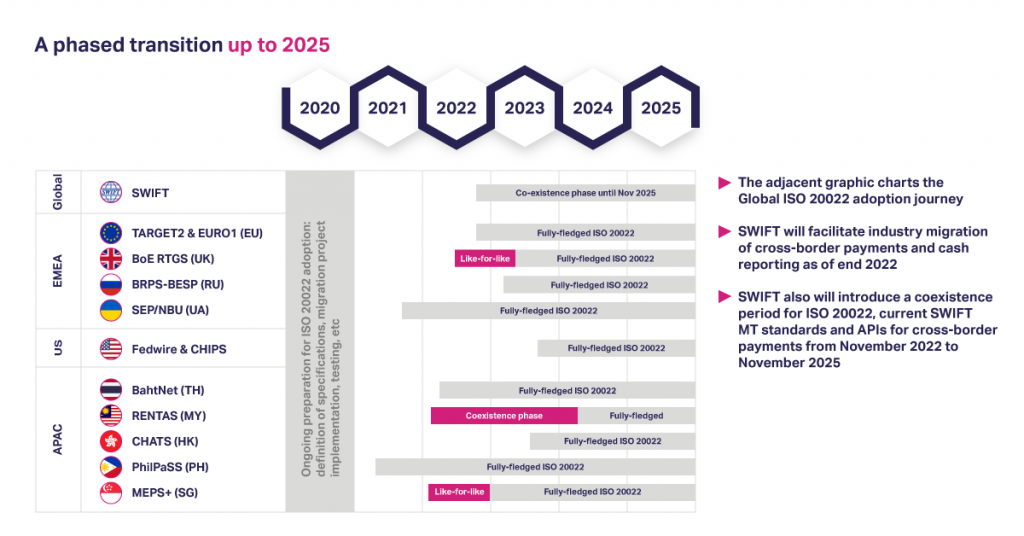

Many market infrastructures have now adopted the task force’s ISO 20022 migration roadmap. Different countries have different timeframes, but by 2025, all reserve currency HVPSs will transition fully to ISO 20022 rich data use, and over 90% of high-value payments worldwide will move on ISO 20022 rails.

Urgent need for engagement

But financial institutions will have to act much sooner than that to prepare. SWIFT will enable cross-border payments and cash reporting businesses to opt into ISO 20022 from August 2022, and implement it for general availability from November 2022.

The success of ISO 20022 harmonisation depends on engagement from the MI community. The standard offers data flexibility and richness to accommodate requirements in different countries – for example, additional debtor identification attributes; remittance information; and purpose code, which denotes the reason for the payment. MIs are developing use guidelines based on HVPS+ to reflect their domestic data requirements and market practices.

It works both ways and financial institutions also need to engage with MIs to adopt HVPS+ now. Failure to do so will put pressure on intermediary banks as they may not be able to pass the rich ISO content from cross border business onto narrow domestic rails.

This could create issues for receiving banks as they will not get the full rich data for screening, delaying settlement.

Benefits of engagement

Market infrastructures migrating to ISO 20022 will benefit in terms of interoperability; ease of compliance; and bridging fragmented payment landscapes and data formats. Just like banks and other financial players, market infrastructures are adapting to changing customer and technological demands. Adopting ISO 20022 standards can keep all their new developments connected by speaking the same language and making them more flexible and resilient.

Global banks operating in multiple regions and with multiple MIs will benefit similarly by using the same language and standard consistently.

Using data-rich payments makes them faster, cheaper, and safer. And removing all the friction between networks enables financial firms to concentrate on adding value to clients and developing their businesses to boost bottom line.

If you want to learn more about the MI migration journey, SWIFT has published an ISO 20022 adoption guide to help MIs meet best practice. SWIFT also has other collaborations with the financial community to harmonise market practices – for example, through the Payments Market Practice Group and Securities Market Practice Group.

How Delta Capita can help

Delta Capita, can help financial institutions with ISO 20022 information and adoption. Delta Capita is a leading global capital markets consulting, managed services, and technology solutions provider, with over 1,200 people across eight main geographies.

We focus on resource augmentation and domain consulting for investment banks, financial market infrastructure and technology acceleration – and we have strong competency and experience in payment solutions. We have a proven track record and are trusted by some of the largest financial institutions.

To see how we can help you maximise the benefits of ISO 20022 adoption, contact Delta Capita’s Global Head of Payments Michael Levens.