By Rita Cool, certified financial planner at Alexforbes

The start of the new year brings ‘tax season’ upon us – a good time to review your financial situation and use any available tax benefits before the end of the tax year on 28 February.

You have until this date to make additional contributions towards a retirement fund, a retirement annuity (RA) or a tax-free savings account (TFSA) to get the benefit in time for your next tax submission. The South African Revenue Service offers generous tax deductions when you make contributions to your RA, pension or provident fund. This means you can save more for retirement, and at the same time, pay less tax.

You can make contributions of up to 27.5% of your total taxable income, up to a maximum of R350 000 per year, and get the tax back. On a contribution of R100 000, if your tax rate is 30% this means that you get R30 000 back in tax and it only reduces your take-home income with R70 000.

There is no tax on growth in a retirement fund or a TFSA. This has a big effect on the long-term compounding of your investments compared to an after-tax investment, where you have to pay tax on growth as well. If you combine the tax-free growth with the tax benefits on the contributions you get money that works for you, not only you working for your money.

Other benefits of saving in these products are:

- The proceeds of retirement funds and RAs are excluded from your estate when you die, which reduces estate duty.

- If you make yearly contributions that are more than the 27.5% or R350 000 per year, you don’t lose the tax benefits on the contributions over the limit. If you are not able to claim the tax allowance before retirement, you can get these contributions over the limit back as a tax-free lump sum at retirement or it can be offset against your retirement income to reduce income tax in retirement.

- The contributions over the limit would form part of your estate if you haven’t received the full tax benefit by the time of your death, but only if your beneficiaries take the amount in cash.

- You can take up to one-third in cash from your RA and retirement funds after 1 March 2021 at retirement, or all of your provident funds before 1 March 2021 if you were 55 years or older on that date. On the current tax table, the maximum tax rate at retirement is 36%. If your retirement income tax rate is going to be higher than 36%, you can access the one-third lump sum at a lower tax rate than receiving it as an income. You can use this cash to supplement the income set up with the two-thirds, which attracts tax. By combining after-tax and taxable income streams after retirement you reduce your overall income tax.

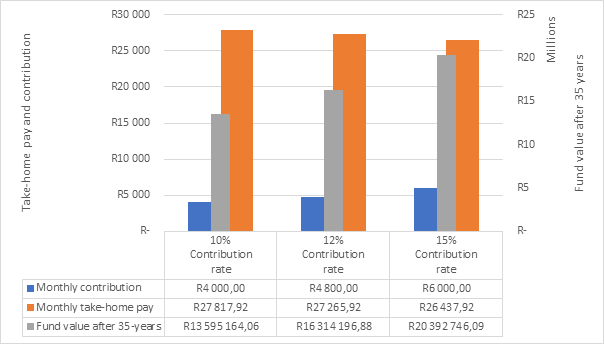

The table below shows the long-term benefits of different contribution rates as well as the impact to your after-tax income if we assume that you earn R40 000 per month.

You can add extra contributions to your retirement fund whenever you want, and there are generally no administration fees charged for these voluntary contributions. One way to do this is to ask your employer if you can increase your contribution rate – if you contribute an additional 5%, your take-home pay will not decrease by the full 5%. Your taxable income would have reduced by 5% and your tax is then also less. This means more money is invested in your retirement savings, and less goes to the tax man.

Another way to make the most of your tax benefits is to open a tax-free savings account, which allows you to save up to R36 000 per tax year and R500 00 over your lifetime, tax-free.

If you can’t make extra contributions to an employer fund, you should consider an RA to make use of the tax benefits. Most annuities have a minimum investment amount to get started.

Speak to your financial adviser if you have questions on the options or if you want to get tax benefits for this tax year.